Key Highlights

Inherited property in Utah is typically valued at its fair market value on the date of death, which becomes the new cost basis for capital gains calculations.

You only owe capital gains tax on inherited property if you sell it for more than its stepped-up basis; no tax is due just for inheriting.

Probate in Utah is necessary for transferring title unless assets were set up to bypass court, affecting timing and complexity.

Tax treatment differs for principal residences, rental properties, and vacation properties in Utah.

Joint inheritance requires dividing capital gains among heirs, reflecting each person’s share.

Accurate documentation and understanding Utah tax laws are crucial for a smooth sale and compliance with tax return requirements.

Understanding Inherited Property and Capital Gains in Utah

When you inherit real estate in Utah, several financial and legal considerations come into play. The property’s value at the time of inheritance is key to determining your potential capital gains liability if you choose to sell. Utah law ensures heirs benefit from a stepped-up basis, helping to minimize taxable income compared to the original purchase price.

You are not responsible for capital gains tax the moment you inherit. Taxable capital gains only occur if and when the property is sold. Next, let’s clarify what inherited property means in this context.

What Is Inherited Property?

Inherited property includes real estate, retirement accounts, securities, and other assets transferred to heirs after the estate of the deceased is settled. Most commonly, a will or legal contract outlines who will receive the property, designating beneficiaries such as family members or close associates.

In Utah, the transfer of inherited assets typically involves probate - a formal court process to validate the will and distribute property. Probate ensures that all outstanding debts, taxes, and the wishes of the deceased are addressed before ownership changes hands. The estate of the deceased may include homes, bank accounts, or investment properties.

Ownership of inherited property becomes official once probate is complete and the title is transferred. This legal process protects both heirs and the integrity of the inheritance, setting the stage for any future capital gains calculations.

Key Differences Between Types of Inherited Properties and Exemptions

Inheriting different kinds of real estate in Utah - such as a principal residence, rental property, or vacation home - can lead to distinct capital gains tax scenarios. The type of property influences not only tax rates but also exemptions and required documentation for your tax return.

While a primary home in Utah may qualify for capital gains exclusions, rental and vacation properties are treated as investment assets, often subject to stricter taxable capital gains rules. Let’s examine these differences more closely.

Principal Residence vs. Rental or Vacation Property

The nature of inherited real estate is crucial to how capital gains are taxed in Utah. A principal residence, if inherited and used as your primary home for two out of five years, may allow for an exclusion of up to $250,000 ($500,000 for married couples) from taxable capital gains.

Rental or secondary properties - including vacation homes - are considered investment assets, meaning gains from their sale are generally taxable at standard federal and Utah rates. Tax return reporting differs as well, with rental income and capital gains from secondary properties subject to stricter documentation and fewer exemptions.

Key points:

Principal residence may qualify for a tax exclusion if lived in for two years.

Rental and vacation properties are taxed as investments.

IRS and Utah rules require separate reporting for each property type.

Documentation of fair market value and sale price is essential.

The Legal Path: Probate & Title Transfer

In Utah, probate is the formal court process required to validate a will and settle an estate's debts before property can be legally sold. The process begins with the court appointing an executor (or personal representative) to manage the assets.

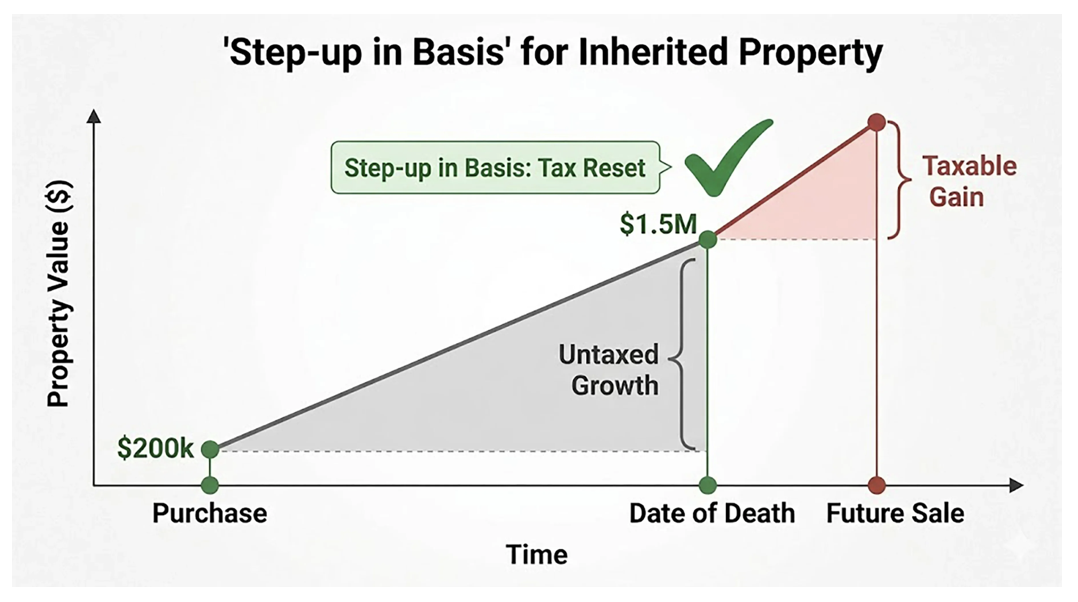

During probate, a professional appraisal is conducted to determine the property’s Fair Market Value (FMV) as of the date of death. This value is critical because it establishes your stepped-up basis, effectively resetting the "cost" of the home to its current value and erasing years of prior appreciation for tax purposes.

Once the court confirms that all debts and taxes are settled, the executor facilitates the Transfer of Title. Legal ownership is officially recorded in the heir’s name, or if the property is being sold directly out of the estate, the executor signs the deed on the estate's behalf. Completing these steps is mandatory to ensure a "clean" title, which is necessary for any future buyer to obtain financing.

Special Considerations for Jointly Inherited Property

When siblings or multiple heirs inherit a Utah property together, they share both the ownership and the tax responsibilities. Under 2026 guidelines, capital gains are divided based on each person’s specific ownership percentage. For example, if three heirs sell a property for a $90,000 gain over the stepped-up basis, each heir reports $30,000 as taxable income on their individual tax return.

Success in joint inheritance requires:

Formal Agreements: Heirs should document how maintenance costs and selling expenses (like the 5-6% agent commissions) are split.

Consensus on Sale: All owners must typically agree to a sale. if a stalemate occurs, a "partition action" or mediation may be required to resolve the dispute.

Reporting Consistency: All heirs must use the same Adjusted Basis (the date-of-death value) on their tax returns to avoid triggering an IRS audit.

What You Need to Get Started with Capital Gains on Inherited Property

Before calculating gains on inherited property in Utah, gathering the right documentation and understanding the property’s current value is essential. Accurate records enable you to establish your cost basis, comply with state and federal tax laws, and avoid legal complications during the sale process.

What Documents do I Need to Collect and Keep when I Inherit Property?

When selling an inherited property in Utah, having the correct documents on hand is crucial to ensure a smooth transaction and compliance with tax regulations. Here’s a comprehensive list of the essential paperwork you should gather before proceeding with the sale:

Certified Death Certificate: This legal document proves the passing of the deceased and is necessary for initiating the probate process.

Probate Documents: Any papers related to the probate administration, including the will and the court's Letters of Testamentary, which grants the executor authority to act on behalf of the estate.

Title Documents: Records that establish ownership of the property, such as the previous deed, which is vital for transferring title to the new buyer.

Appraisal Report: A formal appraisal conducted at the date of death to determine the fair market value, which serves as the new stepped-up cost basis.

Real Estate Disclosure Statement: Completed by the seller, this provides potential buyers with critical information about the condition of the property, any existing issues, and repairs made.

Tax Documents: Retain records of property taxes paid, as these can verify ownership and help in calculating any potential gains upon sale.

Closing Documents: These include any agreements and statements from the closing process, detailing the sale price and expenses incurred during the transaction.

Having these documents organized and readily available not only facilitates the sale process but also prepares you for any questions from the buyer or potential tax inquiries. Being well-prepared ensures that you maximize the benefits of the inheritance while adhering to legal and financial obligations.

Identifying the Property’s Value at Inheritance: The Appraisal

Determining the fair market value of inherited property in Utah at the date of death is essential for setting your new cost basis. This value is usually established through a formal appraisal, which evaluates the property’s condition, location, and current market trends.

The date of death appraisal must be completed by a qualified professional, often at the request of the executor or probate court. This ensures the value is accurate and defensible in case of IRS or state tax inquiries. The fair market value identified in the appraisal is then recorded as your basis for capital gains tax purposes.

Maintaining all appraisal documents and supporting evidence protects you from errors and penalties and ensures compliance with both Utah and federal regulations regarding inherited property.

How are Capital Gains Taxes Calculated on Inherited Property in Utah? A Step-by-Step Guide

Capital gains refer to the profit earned from selling an asset - such as inherited property - above its basis, which is typically the fair market value at the date of death. When you inherit an asset, the Internal Revenue Service allows a “stepped-up” basis, meaning you only pay tax on the appreciation after inheritance, not on gains accrued during the original owner’s lifetime.

Taxable capital gains become part of your taxable income only if you sell the inherited asset for more than its stepped-up basis. For example, if the inherited home’s fair market value is $500,000 and you sell for $550,000, you may owe taxes on the $50,000 gain.

Importantly, you do not owe capital gains tax immediately upon inheriting a property in Utah - taxes are triggered only when a sale occurs, and the profit exceeds the new basis.

Step 1: Determine the Property’s Fair Market Value at Time of Inheritance

The process starts with obtaining a fair market value appraisal for the property as of the date of death. In Utah, this appraisal sets the “stepped-up” basis, the foundation for all future capital gains calculations. The executor or probate court typically arranges for a certified appraiser to assess the property’s worth based on location, condition, and comparable sales.

This date-of-death value becomes your official basis. If you receive a Schedule A to Form 8971 or other estate documentation, use the value listed for consistency with. The adjusted basis for inherited property is always the fair market value at inheritance, not the original purchase price, protecting heirs from paying unnecessary taxes.

If you later sell, your taxable gains are calculated by subtracting this basis from your sale price.

Step 2: Understand the Adjusted Basis (AB)

Determining the adjusted basis (AB) is crucial for accurately calculating taxable capital gains from inherited property. The AB reflects the fair market value at the date of death, serving as the pivotal basis for future property sales. When the estate of the deceased is settled, this value becomes essential for tax return calculations. Factors like capital cost allowance and original purchase price may influence the AB, ultimately impacting any gains exemption that beneficiaries may claim in various tax scenarios.

Step 3: Calculate Your Sale Proceeds and Deduct Expenses

Once you sell the inherited property, your sale proceeds are the final sale price minus closing costs, agent commissions, and other allowable expenses. Utah sellers typically encounter closing fees of 8–10%, listing agent commissions of 3%, and possible transfer taxes.

To calculate taxable capital gains, subtract your adjusted basis from the net sale proceeds. For example, if your AB is $620,000 and you sell for $650,000 after $10,000 in expenses, your taxable gain is $20,000.

Include all expenses on your tax return to minimize your taxable income. Accurate documentation, such as invoices, settlement statements, and receipts, is essential for compliance. This calculation applies for both sole owners and those inheriting property jointly.

Step 4: Divide Capital Gains When Multiple Beneficiaries Are Involved

If inherited property is owned jointly by multiple heirs, capital gains must be divided according to each person’s ownership share. If three siblings inherit a home equally and the total taxable gain is $60,000, each reports $20,000 on their individual tax return.

The division must be documented, and all parties should agree on the calculation method. Disputes may require intervention from a mediator or real estate attorney. Each heir is responsible for reporting their portion and ensuring the basis matches their share.

Jointly inherited property may also involve shared expenses, such as repairs or closing costs, which should be documented and split accordingly. The clarity in division and reporting protects all heirs in case of audits or family disagreements over capital gains.

Timing and Payment of Capital Gains Tax on Inherited Home

Paying capital gains tax on inherited property in Utah is not required immediately after inheritance. The obligation arises only if (and when) you sell the property for a gain above its stepped-up basis. The timing of your sale can influence the tax rate you pay: selling within a year triggers short-term capital gains (taxed as ordinary income), while holding for more than a year qualifies for long-term capital gains rates, ranging from 0% to 20%.

Taxes are reported on your annual tax return in the year the sale occurs. Payment is due when you file, with any taxable income added to your Utah and federal obligations. Consult a tax professional to ensure proper calculation and to avoid penalties for late or incorrect payments. Next, let’s review when this tax is actually owed.

Selling an Inherited Property: Methods and Considerations

Selling inherited property in Utah can be approached in several ways, each with different implications for sale price, timing, and documentation. You may choose to sell by owner (FSBO), work with a discount real estate broker, list with a traditional agent, or accept offers from iBuyers or cash companies. Each method affects your net proceeds and the complexity of the transaction.

Before listing, assess the property’s condition, resolve any outstanding debts or liens, and verify title transfer. The executor plays a crucial role in coordinating the sale and ensuring all paperwork is in order. Factor in closing costs, agent commissions, and transfer taxes when planning your sale. Completing these steps efficiently streamlines the transaction and maximizes your return.

Tips for Handling an Inheritance

Managing an inheritance in Utah requires careful planning and coordination, especially when multiple heirs or complex assets are involved. The following strategies can help you navigate the process with confidence:

Consult a financial advisor or estate attorney to clarify tax implications and selling options.

Keep thorough records of all documentation, including appraisal, title, and tax statements.

Communicate openly with family members to prevent disputes and unexpected delays.

Consider the timing of your sale to minimize capital gains taxes and maximize profit.

Acting as an executor or working closely with one ensures efficient handling of the estate, prompt settlement of debts, and transparent division of proceeds. Accurate documentation and professional guidance help you avoid costly mistakes and capitalize on inherited property in compliance with Utah law.

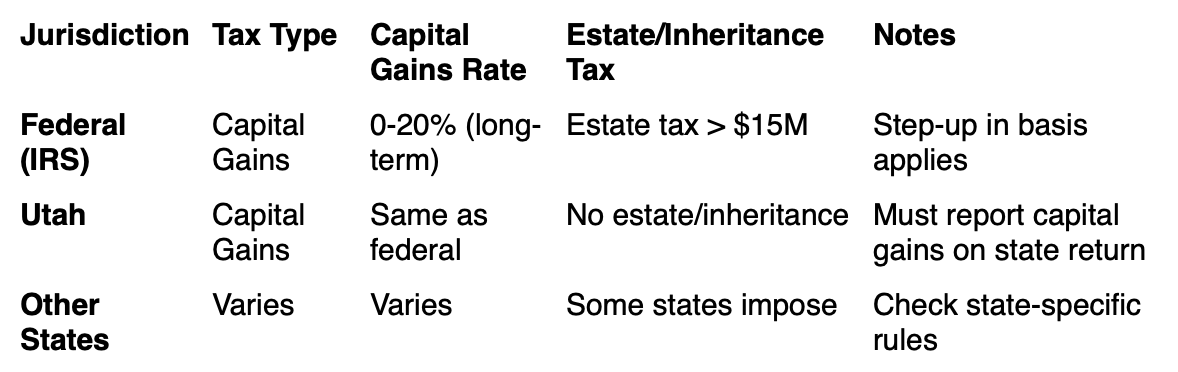

State Capital Gains Tax Differences and Multi-state Inheritance Cases

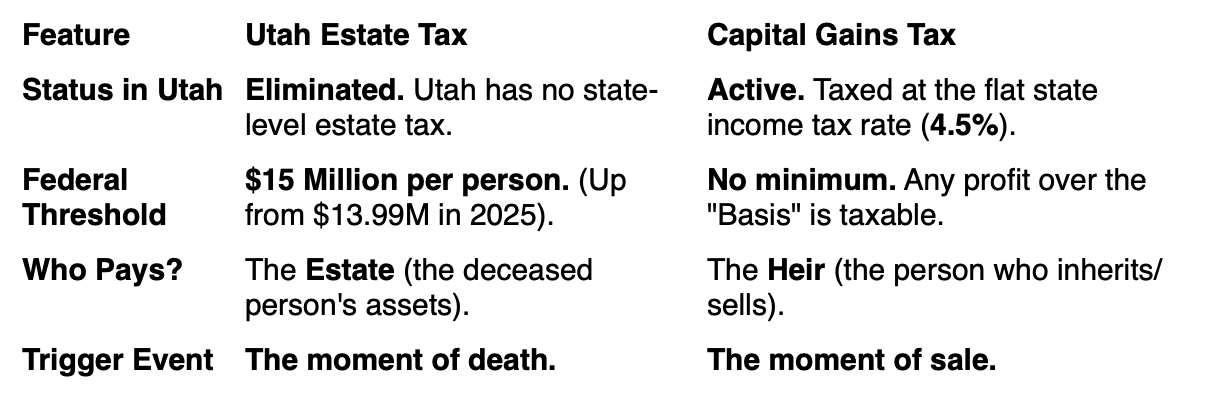

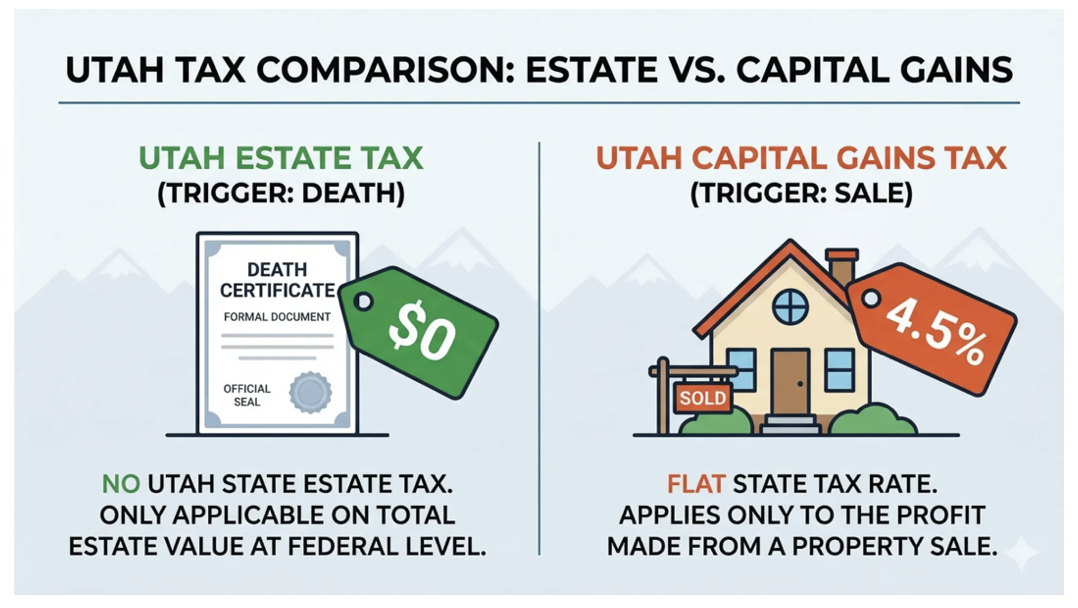

Capital gains tax rates and rules differ between federal, Utah state, and other states, making multi-state inheritance cases particularly complex. Utah does not impose an estate or inheritance tax, but it does require reporting of capital gains on your state tax return. If you inherit property located in more than one state, each jurisdiction’s tax laws may apply, potentially affecting your taxable income and payment deadlines.

Here’s a comparison in text table format:

For multi-state inheritances, consult a tax advisor familiar with the laws in each relevant state to ensure compliance and accurate calculation of all applicable taxes.

Special Considerations for Jointly Inherited Property

When multiple heirs inherit the same property in Utah, dividing both ownership and capital gains tax responsibilities can be complex. Each heir is accountable for their portion of any gain realized when the asset is sold, which must be reflected accurately in each person’s tax return.

Joint inheritance often requires formal agreements to determine how proceeds and expenses are shared. If disagreement arises, a real estate attorney or mediator may help resolve division issues, ensuring compliance with Utah law.

Notable points:

Capital gains are divided among heirs based on ownership share.

All joint owners must cooperate on decisions to sell or keep the property.

Documentation should specify each heir’s percentage and responsibilities.

Family disputes may require neutral third-party intervention.Handling Forced Heirship and Family Disputes Over Inherited Property Capital Gains

Handling Multiple Inheritors and Getting Agreement

When several individuals inherit property together in Utah, reaching consensus on key decisions - such as whether to sell or retain the asset - is essential. Each inheritor’s share determines their portion of capital gains tax liability, which must be documented for tax purposes.

Effective communication and formal agreements facilitate the division of proceeds and ensure everyone understands their rights and responsibilities. If consensus is elusive, engaging a mediator or estate attorney can help achieve resolution and avoid lengthy legal disputes.

Each heir must report their share of the gain on their own tax return. Keeping detailed records, such as ownership percentages and sale documentation, streamlines this process and guards against future challenges. Joint inheritance demands cooperation and clarity to maximize benefits and minimize conflict.

Frequently Asked Questions

Do I have to pay capital gains tax immediately after inheriting a property?

No, you do not pay capital gains tax simply for inheriting property. Taxable capital gains are only due if you sell the inherited asset for more than its stepped-up basis. You report the gain on your tax return in the year of the sale.

How does the adjusted basis work for inherited property in Utah?

The adjusted basis (AB) for inherited property in Utah is set at the fair market value on the date of the deceased’s death. This value becomes your basis for calculating capital gains if you sell the property.

Does the type of inherited property affect how capital gains are taxed?

Yes, capital gains tax rules vary by property type. Principal residences may qualify for exclusions, while rental or vacation properties are taxed as investments. Each type requires different documentation and reporting on your tax return.

What documents should I keep to calculate future capital gains correctly?

You should retain the certified death certificate, property appraisal showing fair market value, purchase price records, seller disclosure, and tax records. These documents help you establish your basis and accurately calculate capital gains when selling.

How do we plan ahead for capital gains from inherited property?

Plan by organizing all documents, consulting professionals, and discussing intentions with family. Understand applicable tax rules and exemptions for each property type. Early planning helps minimize taxes and prevent disputes among heirs.

How are capital gains taxes calculated at the national level vs the state level?

Nationally, the IRS applies federal capital gains rates based on your taxable income and asset holding period. Utah follows federal rates and requires state reporting, but does not impose additional estate or inheritance tax. Utah does impose a capital gains tax when the property is sold.

Does inheriting a principal residence versus a rental or vacation property change how capital gains are taxed?

Yes, principal residences may qualify for exclusions if lived in for two years, reducing taxable capital gains. Rental and vacation properties are taxed as investments and generally do not qualify for the same exemptions, affecting the capital gains calculation.

How do I avoid capital gains on an inherited property?

To avoid capital gains on inherited property, consider using the step-up in basis rule. This adjusts the property's value to its market rate at the time of inheritance, minimizing taxable gains upon sale. Additionally, consult a tax professional for personalized strategies specific to your situation.

If I inherit property jointly with siblings, how are capital gains taxes divided?

When inheriting property jointly with siblings, capital gains taxes are typically divided based on each sibling's share of ownership. Each sibling is responsible for reporting their portion of the gain, calculated from the property's adjusted basis and its fair market value at the time of sale.